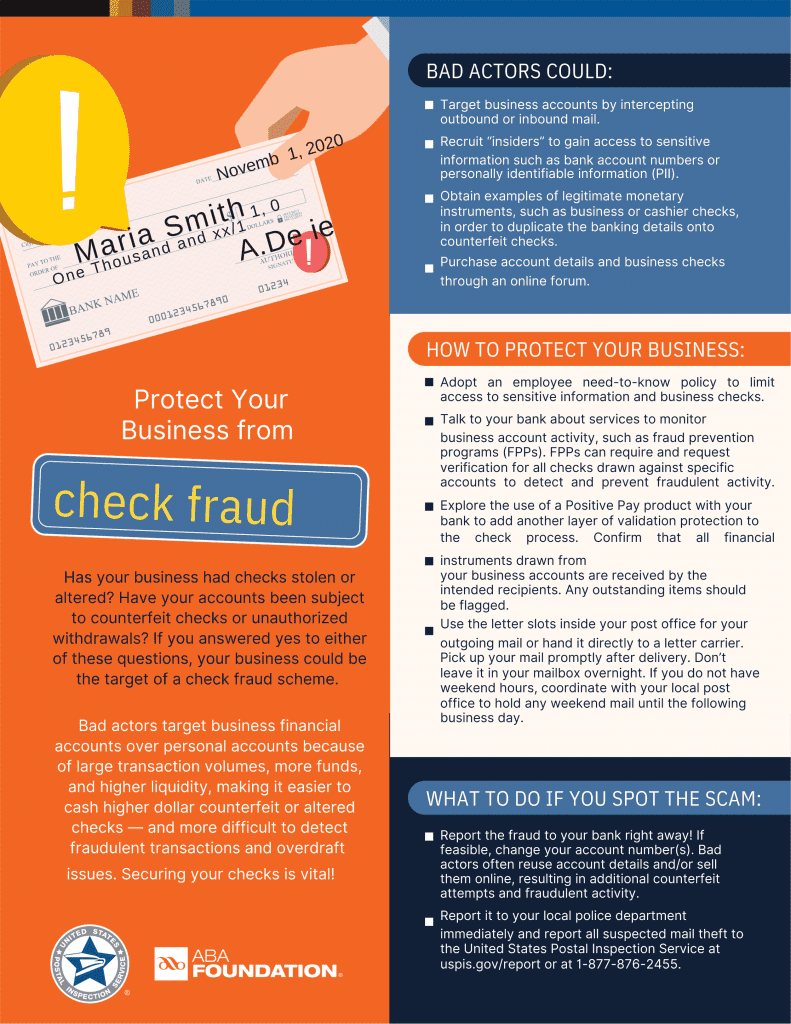

Check Fraud Prevention Tips for Businesses

What is Check Fraud?

Check fraud is one of the largest challenges facing businesses and financial institutions today. With the advancement of computer technology it increasingly easy for criminals, either independently or in organized gangs, to manipulate checks in such a way as to deceive innocent victims expecting value in exchange for their money.

A significant amount of check fraud is due to counterfeiting through desktop publishing and copying to create or duplicate an actual financial document, as well as chemical alteration, which consists of removing some or all of the information and manipulating it to the benefit of the criminal. Victims include financial institutions, businesses who accept and issue checks, and the consumer. In most cases, these crimes begin with the theft of a financial document. It can be perpetrated as easily as someone stealing a blank check from your home or vehicle during a burglary, searching for a canceled or old check in the garbage, or removing a check you have mailed to pay a bill from the mailbox.

Types of Check Fraud:

- Forgery: For a business, forgery typically takes place when an employee issues a check without proper authorization. Criminals will also steal a check, endorse it and present for payment at a retail location or at the bank teller window, probably using bogus personal identification.

- Counterfeiting and Alteration: Counterfeiting can either mean wholly fabricating a check –using readily available desktop publishing equipment consisting of a personal computer, scanner, sophisticated software and high-grade laser printer — or simply duplicating a check with advanced color photocopiers.Alteration primarily refers to using chemicals and solvents such as acetone, brake fluid and bleach to remove or modify handwriting and information on the check. When performed on specific locations on the check such as the payee’s name or amount, it is called-spot alteration; When an attempt to erase information from the entire check is made, it is called-check washing.

- Paperhanging: This problem primarily has to do with people purposely writing checks on closed accounts (their own or others), as well as reordering checks on closed accounts (their own or others).

- Check Kiting: Check Kiting is opening accounts at two or more institutions and using “the float time” of available funds to create fraudulent balances. This fraud has become easier in recent years due to new regulations requiring banks to make funds available sooner, combined with increasingly competitive banking practices.

Check Fraud Prevention Tips

Order checks and deposit slips wisely

- Use an established, respectable source, especially those recommended by your bank, to ensure your checks will process easily through the bank’s clearing system.

- Make sure that your checks include Security Features that will help combat counterfeiting and alteration.

- Make sure you notify your check supplier (and financial institution, if necessary) if a new check order has not been received within a reasonable amount of time after you ordered them.

- Maintain adequate physical security of your checks, deposit slips, etc.

- Secure all reserve supplies of checks, deposit slips and other banking documents in a locked facility. Keep blank checks locked up at all times and limit the number of people with access to your checks. If your checks fall into the possession of unscrupulous employees, you could be liable for substantial losses.

- Change the locks on your facility when an employee leaves your employ

- Never leave checks or bank records unattended in order to assist customers

Issuing and reconciling checks:

- Assign accounts payable functions to more than one person and make each one responsible for different payment areas. This division of responsibility makes it more difficult for employees to tamper with checks and payments.

- Limit the number of official signers. The fewer check signers you have, the lower your chances are of being defrauded.

- Require more than one signature on large dollar check amounts. In this way, any losses you may incur will be low denominations only.

- Immediately notify the bank of any change to your accounts payable process and personnel. You don¹t want former employees who may have secreted some checks from your business to retain authorization to sign them after they have left your employ.

- Separate the check writing and account reconcile functions. Try not to have the same person who balanced the bank statement issue checks. This provides greater safeguards against an employee writing fraudulent checks and covering it up. The reconciler would be able to prevent the crime unless the employees are in collusion.

- Reconcile your account promptly and regularly — quick fraud detection increases the likelihood of recovery. Businesses and personal consumers who do not balance their accounts monthly and don’t find the discrepancies until months have passed, can become liable for losses.